Against the odds, the Greek Parliament passed the necessary austerity legislation as demanded by the EU. In all likelihood it was a grudging acceptance of the harsh conditions and an even an enduring lesson for all politicians with populist proclivities, but its adherence does not bode well for Greece and the EU. Moreover it highlights the dangers of post 2008 growth in sovereign debt and the future of banks too-large-to fail.

Of more immediate concern is whether Greece truly possesses the political will and societal cohesion to fully implement what is expected of them. The extent of what is demanded of them is without precedent except for the onerous conditions imposed on Germany at the Versailles Conference subsequent to WW1 during 1919.

Main picture: Santorini

Let us analyse some of the implications of the raft of requirements to recalibrate their economy.

Foremost amongst those requirements was the reform of the pensions system. All aspects of the Greek pension system defy financial logic. This liability alone has bankrupted Greece. Whereas in most other European countries, the pension equates on average to 40% of one’s final salary, in the case of Greece it amounts to a whopping 95% of their final salary.

As if this did not rip the heart out of the budget, another hare-brained concession was made. Instead of employees retiring in their sixties, they have designated professions as arduous and non-arduous. An employee of an arduous profession is entitled to retire on a full pension at 55 years of age. In their mindless stupidity, the Greek government then conceded that most professions were arduous. Hence they too were accorded these over-generous pensions. Amongst the professions deemed to be arduous were hairdressers, musicians, train drivers and TV presenters.

Yet another uniquely Greek practice exacerbates an already burdened fiscus. Greece has the highest numbers of fictitious people in the world with an age of 110 or older! Deaths go undeclared so pensions are still being paid to people who died over 60 years ago. Some families are drawing 4 or 5 pensions.

Mykonos island

Even in South Africa, Survival Certificates and the use of biometrics has largely eliminated this abuse. How is it possible to do so in a first world country like Greece?

Expecting the EU to fund such egregious abuses is intolerable. As such this issue has been placed at the top of their reform agenda.

Practically what does this mean for Greece’s pensioners?

Will they in their pell-mell rush to comply merely raise the retirement age to 65 and reduce the pension payout to 40% from 95%?

Stunning beaches abound

Hardly likely but with the pensions reform being a critical component of any budgetary reform package, future drawdowns in terms of the bail-out package are contingent on significant progress in this regard.

More plausible will be a slow erosion of percentage payout until the 40% figure is attained. As an inducement to those pensioners between 55 & 65 years of age to recommence working, perhaps a harsher regime will be enacted.

It is entirely possible that the pension payout will be reduced to 40% with immediate effect for that age cohort and then after a year or two eliminated altogether.

The Parthenon

Whatever solution is imposed, it will be a traumatic ordeal for the Greek populace.

As far as employment is concerned, here are some of the statistics relating to governmental jobs:

- Greece has four times the numbers of teachers than Finland. With that ratio of teachers, one would expect Greece to generate the best qualified students instead Finland ranks at the top of the education tables with the Greeks are at the bottom. Despite that dismal performance, the Greek teachers are also the better paid of the two.

- Greek public employment is huge. It is not merely the fact that it is large but more sobering is the level of over-employment prevalent in all departments. It is not unusual to find 45 gardeners for small state gardens and the number of chauffeurs average around 50 per official vehicle

- Over 25% of Greeks in employment are government employees

- The average wage for train workers is €66k and this includes cleaners. Greek railways cost half a billion Euros to run per year. The fares charges are equivalent to one quarter of the employment costs. A previous Finance Minister once facetiously opined that it would be cheaper for all train commuters to instead use taxis at government expense.

- Finally there is an array of fictitious jobs with no purpose. A supreme example of this practice is the Institute for the conservation of the Kopias Lake which employs 1763 people. What rationale is there for employing these 1763 souls as this same lake that has been drained since 1930?

- This practice is so pervasive that an additional 300 of these public institutions have been created over the past decade. For what purpose, nobody actually knows or cares.

To rectify this situation would require retrenching at least 15% of the total working population of Greece in one fell swoop. Due to the penury of the Treasury, any payout would have to be frugal at best.

Finally the level of tax compliance is abysmal.

- It is estimated that of all 300 parliamentarians, all are defrauding the tax man in some way

- Of the professionals such as doctors, 25% pay tax as they wilfully declare too little income

- At least 25% of Greeks do not pay any taxes on private income

If these examples do not illustrate the dire financial situation that the Greek people and Styzia, the ruling party, finds themselves in, nothing will.

While the facts as enumerated above are undoubted indisputable, what they do not highlight are issues germane to this discussion: debt, financial markets and austerity generally and in Greece’s case in particular.

Beneath the sanctimonious accusations by the Banks regarding Greek overspending lies a large dollop of hypocrisy. Are not all prudent lenders supposed to assess the financial ability of the country to repay those loans? Prudence dictates that no further advances be made when the Gross Government Debt reaches critical levels which generally is recognised as being no more than 60%.

Clearly not.

Instead of insisting that the European Banks with their lackadaisical approach to credit control accept a modicum of guilt and write down the debt, the EU has insisted that the full amount be repaid.

With the best will in the world and the most stringent compliance with the conditions imposed, I am of the opinion that Greece will be unable to fulfill her obligations. Possibly it is a moot point, but I remain wholly unconvinced of their ability to do so.

What is disconcerting is that subsequent to the financial crisis of 2008, sovereign debt has exploded world-wide. This has placed many other EU countries at risk. Being a minnow in the European context – Greece represents 2% of the GDP – there is no risk of a financial collapse spreading its contagion across the continent.

Queues outside Greek ATMs

Instead it is the risk of over indebtedness by fellow EU members where the risks are greatest.

Moreover by Europe having at its heart a single currency, it is singularly susceptible to repetitive shocks when the value of the single currency – the Euro – is out of sync with the economic fundamentals of its constituent parts. As economist Stephen Keen has re-iterated, “An exchange rate is a country’s ultimate “international price” and [by] removing its cushioning and balancing role, [it] completely eliminates the capacity for smooth adjustments to circumstances.”

It was not that the EU members were blind to his sage comment when opting for a single currency. Instead they chose to wilfully ignore its consequences. To address this issue would have meant that the single currency project would have been dead in the water – stillborn. In order to prevent this divergence would have had to renounce their independent economic and fiscal policies.

The Federalists envisaged a step-by-step convergence by stealth approach. This approach might well now be ship-wrecked on the rocks of inconsistent financial policies or economic performance.

What has been most disheartening since the 2008 crash is that in spite of a world-wide 40% increase in debt since that date, the net effect has resulted in a dismal failure to encourage economic growth which it was designed to do. Whether it has been Shinto Abe in Japan or Janet Yellend at the Fed in the USA, the result has been the same: increasing levels of debt without the commensurate increase in economic growth.

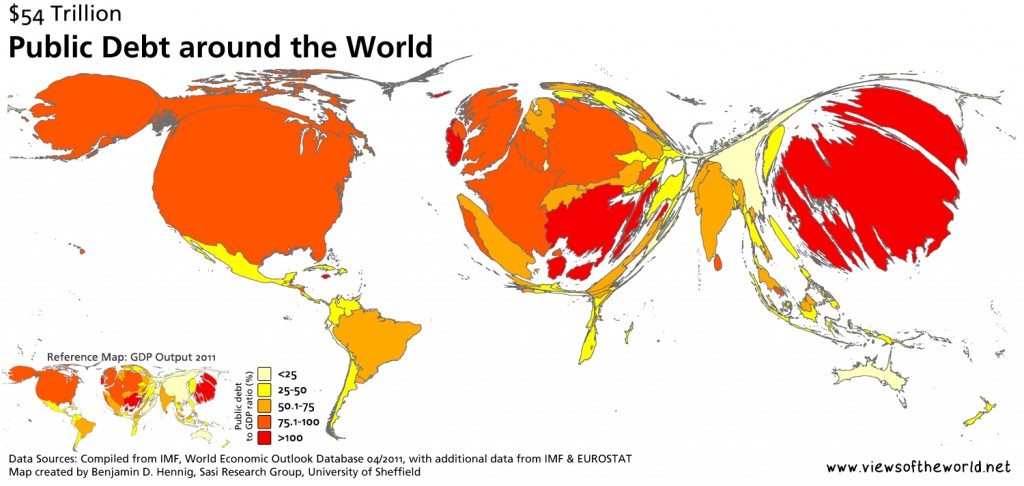

Public debt around the world

It is now estimated that total global debt – both governmental and private – amounts to a staggering 300% of global GDP. Like the ineffectiveness of reduced interest rates which have made no discernible difference except to create a huge asset & debt bubble, it will ultimately – like all ephemeral children’s bubble spray – burst with dire economic consequences.

All of this is a moot point but what is becoming an ever more contentious debate is whether the banks are aiding or hindering economic growth.

The debt trap

Until recently this would not have been in contention. It was readily accepted that role of the financial sector was to mobilise savings, improve resource allocation through correct pricing of debt, facilitate the management of risk and to promote financial stability amongst others.

Upon closer inspection, the IMF has questioned this immutable logic and whether this is always so.

The IMF points out that “there are costs as well, particularly at high levels of financial development. In fact, there can be instances where there is ‘too much finance’, that is, instances where the costs outweigh the benefits.”

Why the sudden volte face on the value of financial services? The growth in Banking’s share of GDP has incremented to a significant 20% globally. Whereas Banking should be the facilitators of economic development, it has become the driver; it should be the slave and not the master. Over the preceding three decades, the world has witnessed a significant shift in this position and viewing it retrospectively, one recognises the consequences of its devastatingly parasitic nature.

The disaster that is Greece could, with the effluxion of time, provide momentum to these forces of re-focusing on the true role of the banks and renewal of their mandate.

For all our sakes, let the re-alignment of the role and modus operandi of the lending institutions together with their assiduous application of the prudence principle prevent yet more sovereign defaults.

If not, the mantra of those opposed to continued support of banks will only be stilled by comprehensive and mandatory lending criteria and intrusive regulatory overview, neither of which is desirable.

Perhaps that is, as the IMF now contends, the only viable solution.

This certainly makes sense of why Greece is in the mess it is in!